2023 Review: What's the state of the VLE market in UK higher education?

Since 2021, I have been providing an annual review of the Virtual Learning Environment (VLE) market in UK higher education, aiming to highlight trends, notable developments, and evolving market shares.

Each year I’ve broadened the scope of my analysis to include more universities and this year is no exception. In my 2023 review, I’ve conducted research and analysis on 247 UK universities, a significant increase from the 179 included last year. Although changing totals aren’t great for year-on-year comparison, this year I’m able to provide a more comprehensive overview of the market.

As I’ve been at pains to point out in previous years, shifts in market share typically represent a slow evolution rather than significant annual changes. So this year I’ve sought to look at market share from different angles to provide a more nuanced perspective.

It is important to note that this market is somewhat oligopolistic, dominated by four main VLE products: Blackboard, Brightspace, Canvas, and Moodle. There isn’t much dynamism in terms of new entrants significantly disrupting that established order .

However it’s worth mentioning that this year has been more interesting than most in terms of product developments. The increasing integration of AI has led to new features and partnerships, and ultimately, more to discuss.

What are the market share headlines?

The overall trends in 2023 reflect a continuation of the patterns observed over the past few years. Moodle and Blackboard still hold the largest shares of the overall market, but this reflects their past dominance. Both remain uncompetitive in terms of gaining new university clients.

This year, as in previous years, Canvas and Brightspace have sustained their year-on-year growth, successfully being adopted as core VLEs by new university clients.

Canvas is experiencing the strongest growth in adoption among UK universities and several institutions have started using it this year. The number of universities choosing Brightspace as their VLE also continues to grow.

While Blackboard has managed to secure some contract renewals with existing UK university clients, it continues to lose clients and struggles to acquire new ones. Moodle appears similarly unappealing to UK universities looking for a new VLE.

The market momentum remains with Canvas and Brightspace, and the decline in Blackboard's market share, evident for several years now, continues. The company just doesn’t seem to be able to turn the tide.

What’s the overall market share?

As I mentioned earlier, the overall market share is based on research and analysis of 247 UK universities, ranging from large to small institutions.

It's important to note that the figures relate to the core VLE used by universities for the majority of their students. While several universities use multiple VLE products, they all have a primary VLE for the bulk of their students. In cases where two or more VLE products are used, the others are typically for smaller, specific purposes, such as exclusively for online programmes.

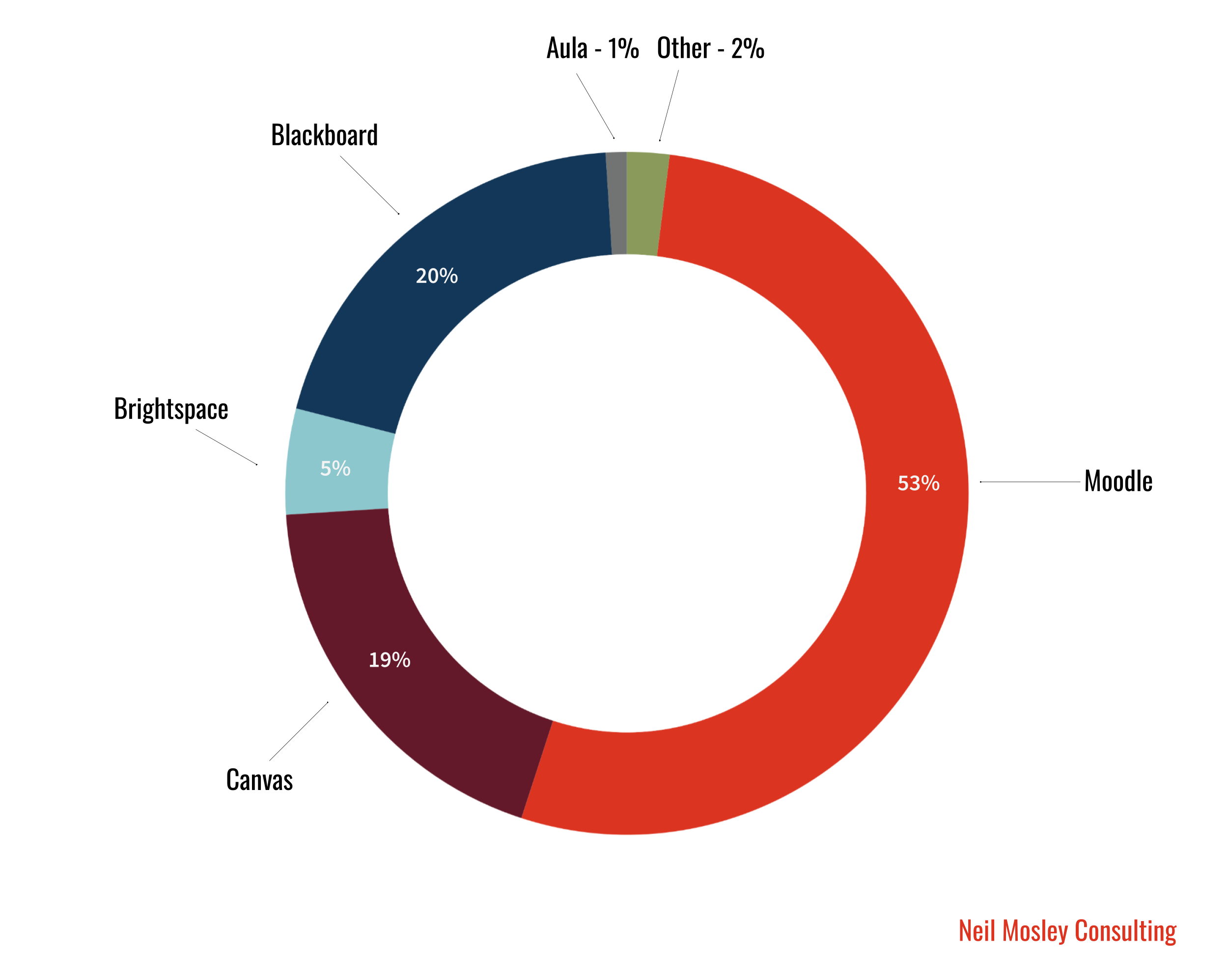

Proportion of VLEs being used by 247 UK universities researched as of the end of 2023.

Due to the expanded scope of my research this year, direct year-on-year comparisons are challenging. However, the increased numbers, along with gains from Canvas, show that Blackboard is now very close to being ousted as the second-largest player in the market.

However, the overall market share picture only tells you so much, as it spans a wide variety of institutions, from large & prestigious to small & specialised.

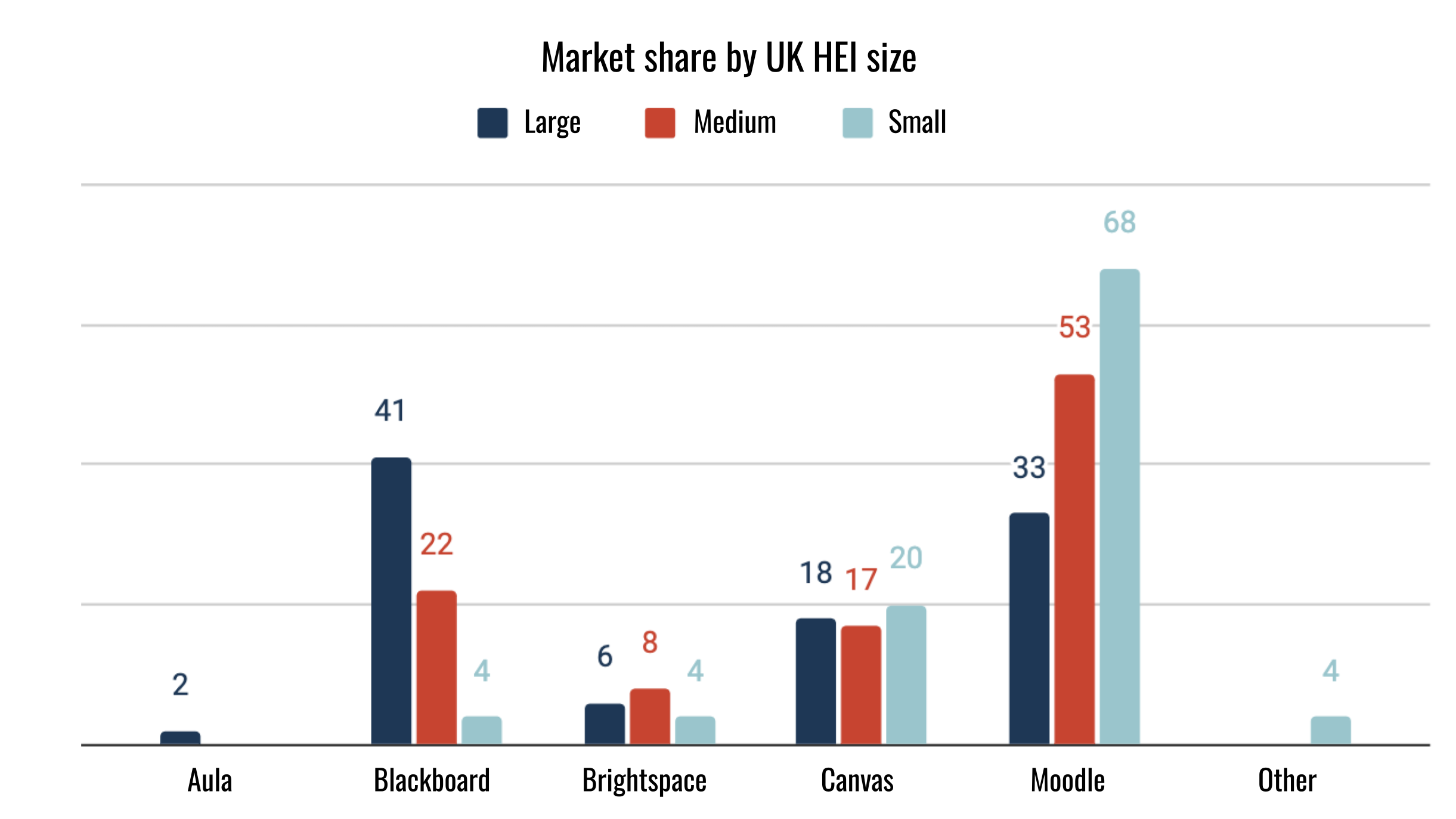

Analysing market share by size of institution offers a more rounded picture. This year I’ve segmented universities based on their total student numbers within the UK, using the latest HESA data from the 2021/22 academic year.

The segments are as follows:

Small: fewer than 5,000 students

Medium: 5,000 to 15,000 students

Large: over 15,000 students

What is most striking across these segments are the fluctuations in Blackboard's and Moodle's market shares, contrasting with the more consistent shares of Canvas and Brightspace across all three.

Blackboard has the largest market share in the large UK university segment, but this significantly decreases in the medium and small segments. Whereas the opposite is true for Moodle and it has the biggest market share (68%) in the small segment.

The consistent shares of Canvas and Brightspace demonstrate their growth across all segments, having been adopted by small, medium, and large UK universities in recent years.

Focusing on large UK universities gives a more rounded view of Moodle than the overall picture suggests. Moodle's substantial adoption by relatively small universities skews the overall perspective, potentially presenting them as a more dominant player than they are. In reality, 70% of the small UK universities using Moodle have fewer than a thousand students.

A rough estimation (and this is not an exact figure) based on HESA data, suggests that around 40% of all UK-based students use Moodle. While still significant, this percentage is smaller than what their overall market share might imply.

What about market share by UK Region?

One other way to look at market share is by UK region. This analysis is complicated by the fact that the number of universities in England vastly exceeds those in Northern Ireland, Scotland, and Wales.

Unsurprisingly, therefore, England's market share broadly reflects the overall picture. However, in Scotland, Moodle (40%) isn’t as far ahead of Canvas (27%) and Blackboard (20%).

Wales is probably the most interesting region to observe, as it strongly favours the two traditional and longstanding players, Moodle (55%) and Blackboard (36%). Swansea University, which uses Canvas, is the only university in Wales to have opted for one of the other market players.

Lastly, in Northern Ireland, Canvas has the largest share as it’s used by two of the three NI universities included in this analysis.

What about the companies themselves?

While the overall market share might not show significant changes from last year, there have been developments within the companies behind these VLE products that merit attention, as well as notable product developments. These things could influence market shifts going forward.

Time doesn’t allow for comprehensive deep dives here, but I want to pick out things that have caught my attention or have felt noteworthy in the past year among the main company players.

Moodle

Last year, one of the most significant pieces of news in edtech was Moodle's founder and CEO, Martin Dougiamas, stepping down and transitioning to a Head of Research role. This marked the end of a 24-year period as CEO and feels like the end of an era. He will now focus on research and innovation, with AI playing a significant role in that.

Scott Anderberg was appointed the new CEO towards the end of 2023. Scott brings years of experience in higher education, edtech, and online learning. His most notable role was a 15-year period at Pearson, including time as Vice President of their OPM arm, Pearson Online Learning Services (POLS).

This move seems geared towards making Moodle more competitive. There’s a lot of love for Moodle and its ethos in the UK, but this alone isn’t going to turn the dial for a product that’s grown less competitive. Ultimately that matters and you can only live on the fumes of positive sentiment for so long.

Product-wise, Moodle launched Moodle 4.3 in 2023, building on the 2022 release of Moodle 4.0. The messaging and focus again appears to be on enhancing user experience rather than introducing significant new features.

There also seems to be a relative lack of new AI-related features compared to other VLEs. Moodle has identified key areas for AI's positive impact and developed plugins, but there's a sense they've been slower to adopt and integrate AI extensively. Time will tell whether that further hinders their competitiveness or if their strategy will pay off, but it certainly differentiates them.

Blackboard

It has been over two years since Blackboard was acquired by Anthology, and, similarly to Moodle, they also appointed a new CEO last year, Bruce Dahlgren.

In the UK, recent activity has focused on transitioning clients from Blackboard Learn to Blackboard Ultra. A significant proportion of UK universities have either completed this move or are in the process of doing so.

I have previously discussed the illusion of moving to something new with Ultra, when in fact it’s been around since 2016. Nevertheless this has given the company and UK universities something to focus on in recent years and may have had an influence on those universities tempted to look elsewhere.

Despite broader changes in the parent company and the shift to Ultra, Blackboard continues to see a decline in its UK university client base. This trend is echoed in other regions, with notable examples like the University of Southern California switching from Blackboard to Brightspace.

Although the product remains uncompetitive, efforts to enhance it include the introduction of new AI-powered features. These are encapsulated in the AI Design Assistant, a feature that’s only available in Learn Ultra.

The feature primarily focuses on assessment, offering test question generation from provided content and AI-assisted rubric creation. The assistant also offers some potential shortcuts for educators, such as recommendations on course structure, titles, descriptions, and royalty-free images related to the course content.

Anthology has also introduced what they describe as an authentic assessment feature. This feature appears to combine learning objectives, course content, and Bloom's taxonomy, producing “prompts aligned to Bloom’s Taxonomy that promote critical thinking like analyzing, creating, and evaluating”.

This is probably not the place to discuss what I think about the formula “pedagogical pyramid representation + edtech product development = …….“ but let's just say I’m not totally convinced.

However, it seems evident that Anthology is trying to rapidly leverage the opportunities AI provides to develop Blackboard into a more appealing product.

Canvas

Instructure has had a successful 2023, with a number of UK universities adopting Canvas for the first time. In a couple of instances, Canvas has been selected by universities needing to replace a VLE from a newer market entrant that hasn’t been able to run the course. Although not yet announced, they have also been chosen by a large Russell Group university, which represents a significant success. This adds to their roster of Russell Group university clients, including Birmingham, Liverpool, Newcastle, Oxford, and Queen's University Belfast.

One of the most eye-catching pieces of news this year was the partnership announced between Instructure and Khan Academy. This collaboration aims to integrate Khanmigo, an AI tutor and teaching assistant, with Canvas.

Khan Academy has embraced the potential of AI, while HE-focussed products seem to have been more cautious, perhaps keen to keep in step with the HE sector's more conservative response. In that sense this feels like a good match, offering more adventurous universities an opportunity to experiment in ways they might not have had otherwise.

Another promising AI feature is the introduction of conversational AI into Instructure's analytics product. There has been increasing interest in VLE analytics capabilities, and this functionality, combined with more sophisticated AI interfaces for data interaction, is an appealing combination.

One last development of note is Instructure’s acquisition of Parchment, an academic credentialing platform. This move seems well-timed in an environment where there is more experimentation with credentials, whether that be alternative, micro, or stackable. It provides Instructure with a platform within their ecosystem to respond to trends and the evolving landscape of credentialing.

Brightspace

Brightspace from D2L, while perhaps the least well-known of the main VLE products in UK higher education, is expanding its presence both in the UK and in other regions, such as the US.

The current CEO, John Baker, founded the company over 20 years ago while he was a 3rd year undergraduate student, and with Martin Dougiamas stepping down; he's the last CEO/Founder standing among this group of companies.

This year, D2L has incorporated several AI-powered features into Brightspace, focusing on formative assessment and help and assistance. A new generative AI feature supports educators in creating practice questions for students, and a new virtual assistant uses AI to provide contextualised help and documentation.

My impression is that D2L has been a bit more restrained than others in implementing AI features, but they have been doing valuable work before 2023's AI frenzy. In 2022, Brightspace was enhanced to support the automatic generation of closed captions for uploaded videos in various languages. This is my kind of feature, understated but incredibly useful and valuable.

D2L has also formed some interesting partnerships this year. Continuing with the AI theme, one notable partnership was with Copyleaks, who are essentially an AI detection company. This certainly differentiates them from other players and aligns them with strategies adopted by some universities that focus on addressing threats to assessment methods through detection. This is a controversial and well debated topic, but I remain to be convinced of the efficacy of AI detection tools.

Another significant partnership announced last year was between D2L and Quality Matters (QM). Although less well-known in the UK, QM is a prominent quality assurance organisation for online learning, mainly known for their rubrics. At this stage it’s hard to tell what this partnership will deliver, but it’s one that aligns well with the growing emphasis on developing online course portfolios.

What about the rest?

In respect to other products in the VLE market, Aula is the only one of note in terms of market share. Last year, I discussed its demise as a market player following its acquisition by Coventry University. Before the acquisition, Aula was used by three UK universities (including Coventry), but since then, one of these has switched to Canvas.

Coventry University seems to have invested in the Aula platform, and there have been product developments over the last year. However, the future of Aula remains uncertain. At the end of last year, it was reported that Coventry University would need to make nearly £100 million in cuts over a two-year period. While plans are yet to be finalised, mentioned was made that along with other measures, they are "broadly expected to include contractor fees for digital services projects, software purchases, and other digital services operating costs."

Whether this in any way relates to Aula is hard to say, but Coventry is unique in being the only major university in the UK that owns and operates its VLE. There have been question marks in the past over the financial sustainability of such a move, and these are made more stark in the current financial climate.

In other news, Multiverse's acquisition of Eduflow has effectively removed Eduflow from the VLE market landscape. Prior to this, Eduflow had been used as the VLE for one small UK university.

To sum up…

In the UK HE VLE market, there are two dominant incumbents and two seemingly serial winners of new VLE implementations. The market is gradually shifting towards the latter, and unless Blackboard and Moodle improve their competitiveness, it is likely that next year will see Canvas take second place in the overall market share, with Brightspace continuing to grow market share.

Recent years have starkly highlighted the challenges of breaking into this market and the risks associated with adopting products from newer entrants. The experiences of Aula and Eduflow have forced some UK universities to make changes they would not have otherwise considered. Given the current financial climate in UK higher education, it's hard to imagine universities being eager to choose newer entrants who are less able to compete with the incumbents on price in the coming years.

AI developments have added some dynamism to the VLE space in 2023, and we can expect to see more product developments in 2024. A key challenge will be to avoid feature bloat due to overzealousness and ensure that new features and functions provide real value. Edtech is rife with simplistic and vacuous translations of educational ideas and research into product developments. Without input from people who really know their stuff when it comes to learning and teaching, some new AI-powered features will follow a similar path.

This year, there has been a bit of discussion about the future of the VLE, something we briefly touched on in our 'Online Education Across the Atlantic' podcast episode that explored the impact of AI on the VLE market. I have to say I’m in agreement with Phil Hill who said that “it’s not wise to bet against the VLE market centrality” and nothing I’ve seen this year convinces me otherwise. The VLE remains central to what UK universities do and increasing moves into online education, microcredentials and blended & flexible learning don’t threaten that.