International online students in UK higher education: What the 2024–25 TNE data reveals

Having recently posted an analysis of UK online student enrolments, it is time to take a look at international equivalents, namely transnational education (TNE) online student enrolment trends based on the latest student data release by HESA for 2024–25.

UK higher education’s focus on TNE in recent years has been significant, driven by a combination of factors. These include growing constraints on international on-campus recruitment caused by policy changes that compel providers to diversify, developments within countries such as India that enable branch campus opportunities, and the UK Government’s international education strategy, which aims to grow education exports.

TNE is not simply an area of greater policy focus, but also of increased activity. This is demonstrated by growth in the number of TNE students at UK institutions overall. There has been an increase from a total of 489,285 TNE students across all levels and types of provision in 2020–21 to 669,950 in 2024–25, as several institutions have been active in developing their overseas operations and increasing their TNE student numbers.

In 2024–25, online distance learning students made up approximately 21% of total TNE students across all levels, a not insignificant proportion overall.

Just as with UK online student enrolments, there are two main markets, undergraduate degrees and postgraduate taught degrees. This analysis will examine both in turn, starting with the online undergraduate degree TNE student landscape.

International online undergraduate degree students: 2024/25 HESA trends

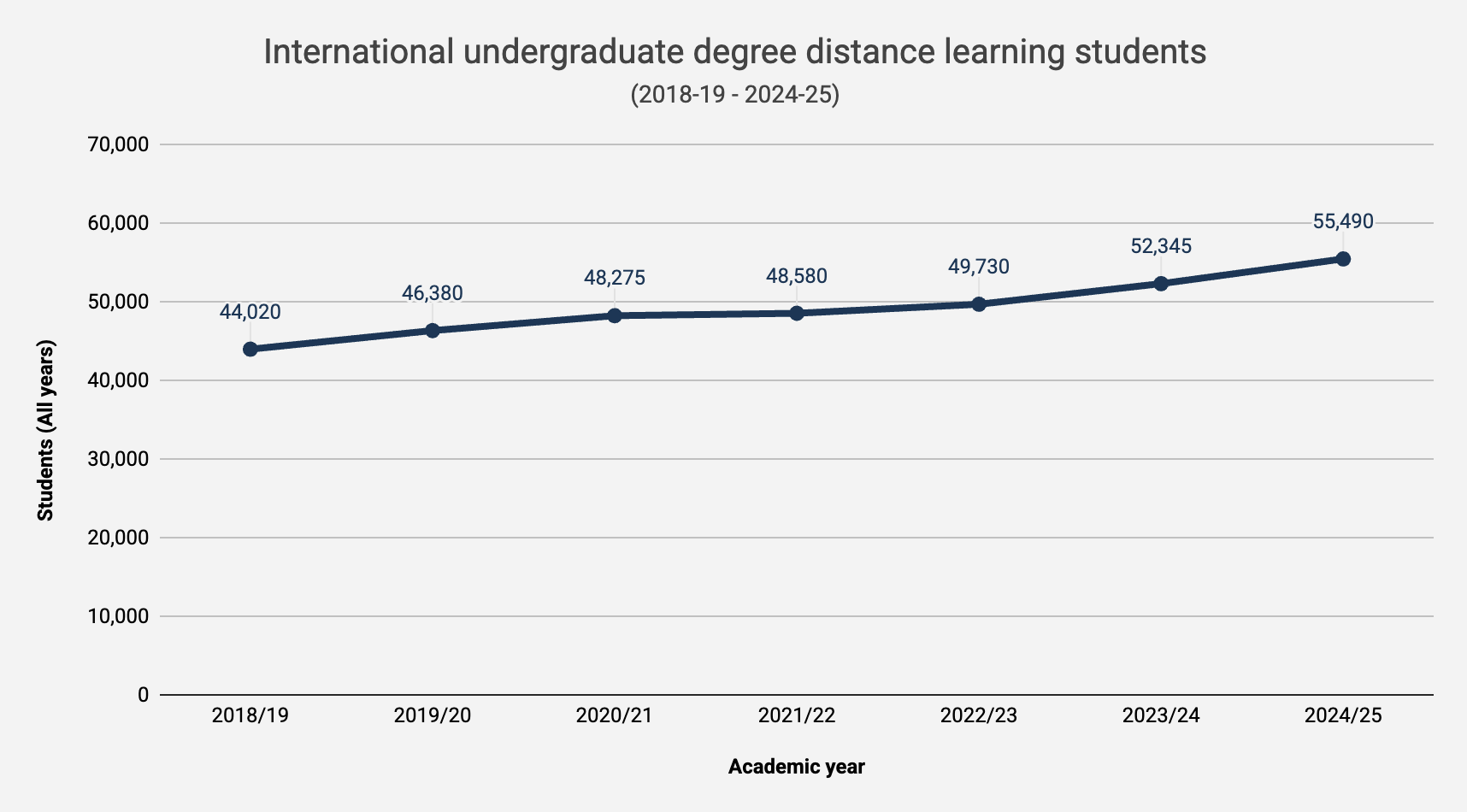

The 2024–25 HESA student data shows the most significant year-on-year increase in TNE distance learning undergraduate degree students over the past decade. The total number of international online undergraduate degree students increased by 6% in 2024–25, equivalent to 3,145 students. This continues the trend of year-on-year growth since 2019–20.

However, it is fair to say that growth is highly concentrated, both in terms of regions and higher education (HE) providers. Unfortunately, the data for TNE students is far more limited than the main HESA student record and presents some challenges in offering deeper insights, but it is possible to explore student enrolment trends by broad international regions.

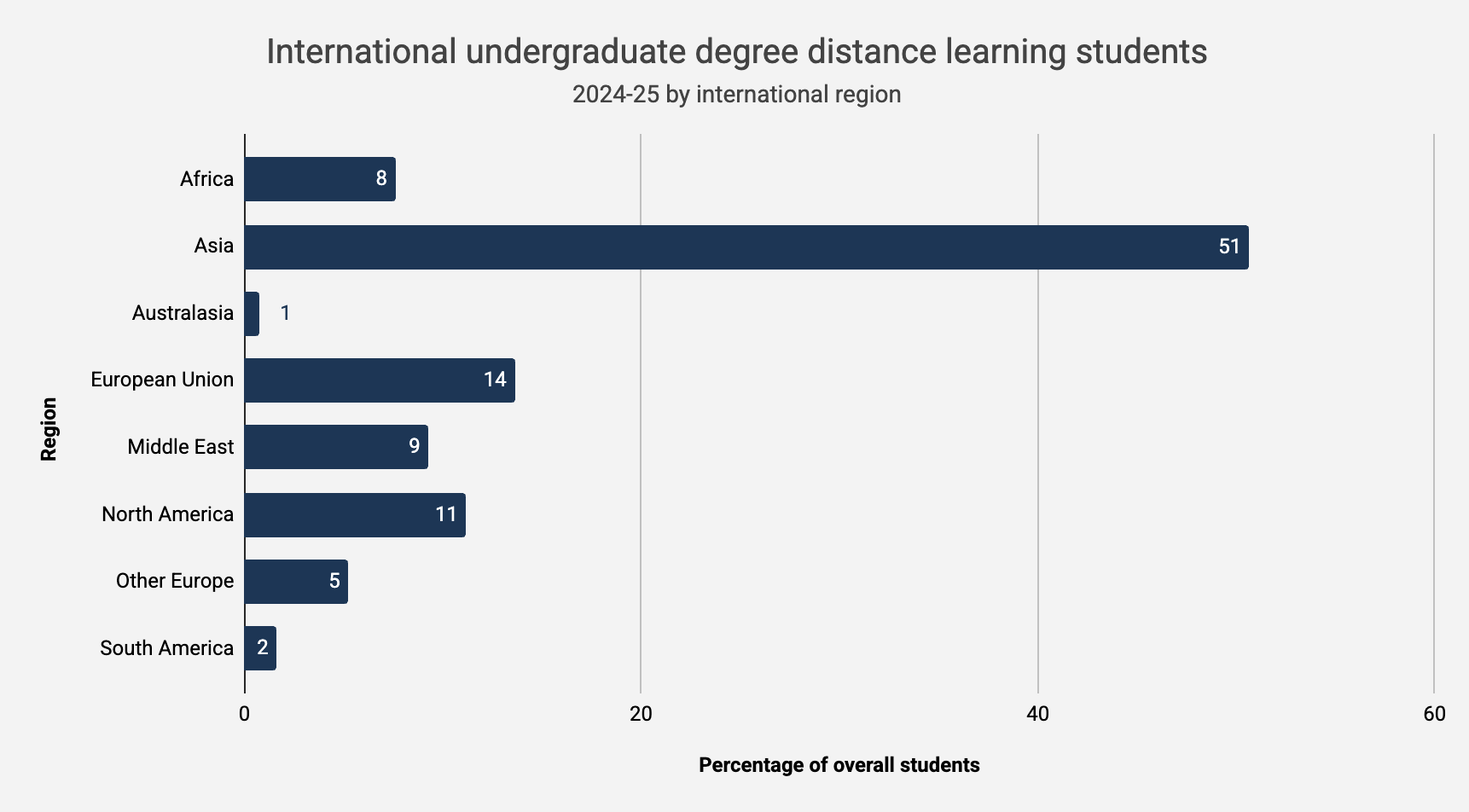

This highlights how concentrated the number of online undergraduate degree students is. As of 2024–25, over 50% of these students are based in Asia, with smaller concentrations in the EU and North America, as the data below shows.

Over the last five years of reporting, the regions that have contributed most to growth have been Asia and the Middle East. While growth in the number of students in Asia has largely been steady year on year, the number of students in the Middle East has grown at a far more significant rate, with strong annual percentage increases from a smaller base. These regions are the main drivers of growth this year, with both contributing increases of over 1,000 online undergraduate degree students.

International online undergraduate students by provider

Just as student numbers are concentrated by region, they are also concentrated by HE provider, with only seven universities with over 1,000 students. Even among these institutions, the University of London, with 29,000 students and over 50% of all online undergraduate degree TNE students in 2024–25, dwarfs the rest.

Correspondingly, the most significant increases in student numbers have been among these universities, with the University of London, Oxford Brookes University and the University of Hertfordshire recording the largest year-on-year rises. Beyond these, the University of Derby, Coventry University, Anglia Ruskin University, the University of Essex Online and the University of Leicester also recorded increases numbering in the hundreds.

The following universities, by student numbers, represent the leading UK institutions operating in the online TNE undergraduate degree market.

Top UK universities by number of international online undergraduate degree students

University of London - 29,825

Open University - 6,325

Oxford Brookes University - 4,055

University of Hertfordshire - 2,935

Arden University - 1,905

University of Essex Online - 1,700

Edinburgh Napier University - 1,435

University of Derby - 975

I deliberately use the term markets because there is always a danger of interpreting online TNE activity as a large global B2C market in which UK HE providers offer online degrees to a uniform international audience. The reality is quite different, and the students represented within the universities listed here are not evenly distributed across regions. For example, over 50% of the Open University’s students are based in the EU and over 60% of Edinburgh Napier University’s students are based in North America.

These institutions remain the same top seven as last year and, in the majority of cases, represent those invested in online undergraduate provision in both UK and international markets. While some other institutions are building up their student numbers, I anticipate that these universities will continue to be the most prominent recruiters of online undergraduate degree students internationally in the coming years.

International online postgraduate degree students: 2024/25 HESA trends

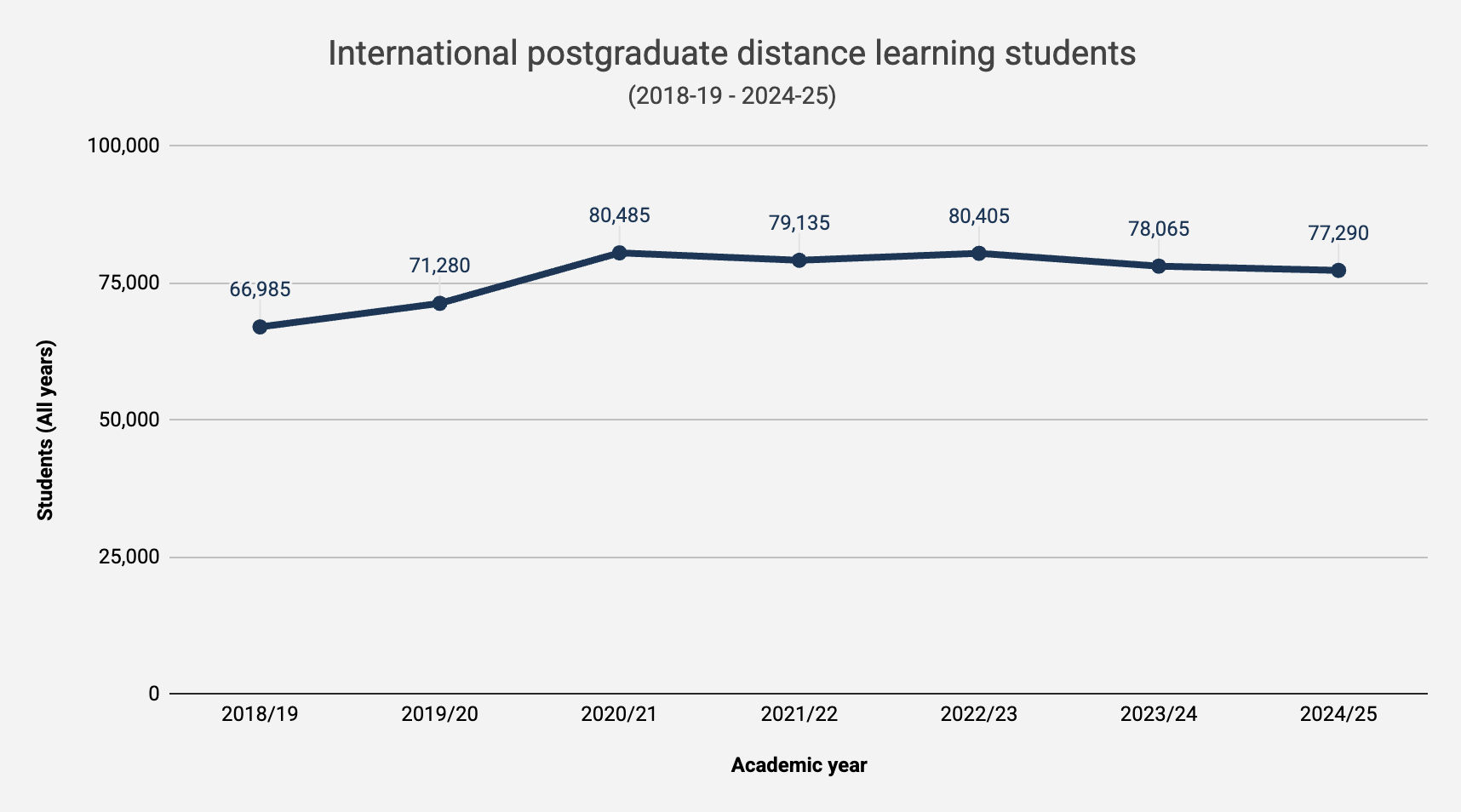

Whereas online TNE undergraduate degree student numbers have followed a year-on-year upward trend, postgraduate numbers have fluctuated and, in 2024–25, fell slightly by 1% or 775 students to 77,290.

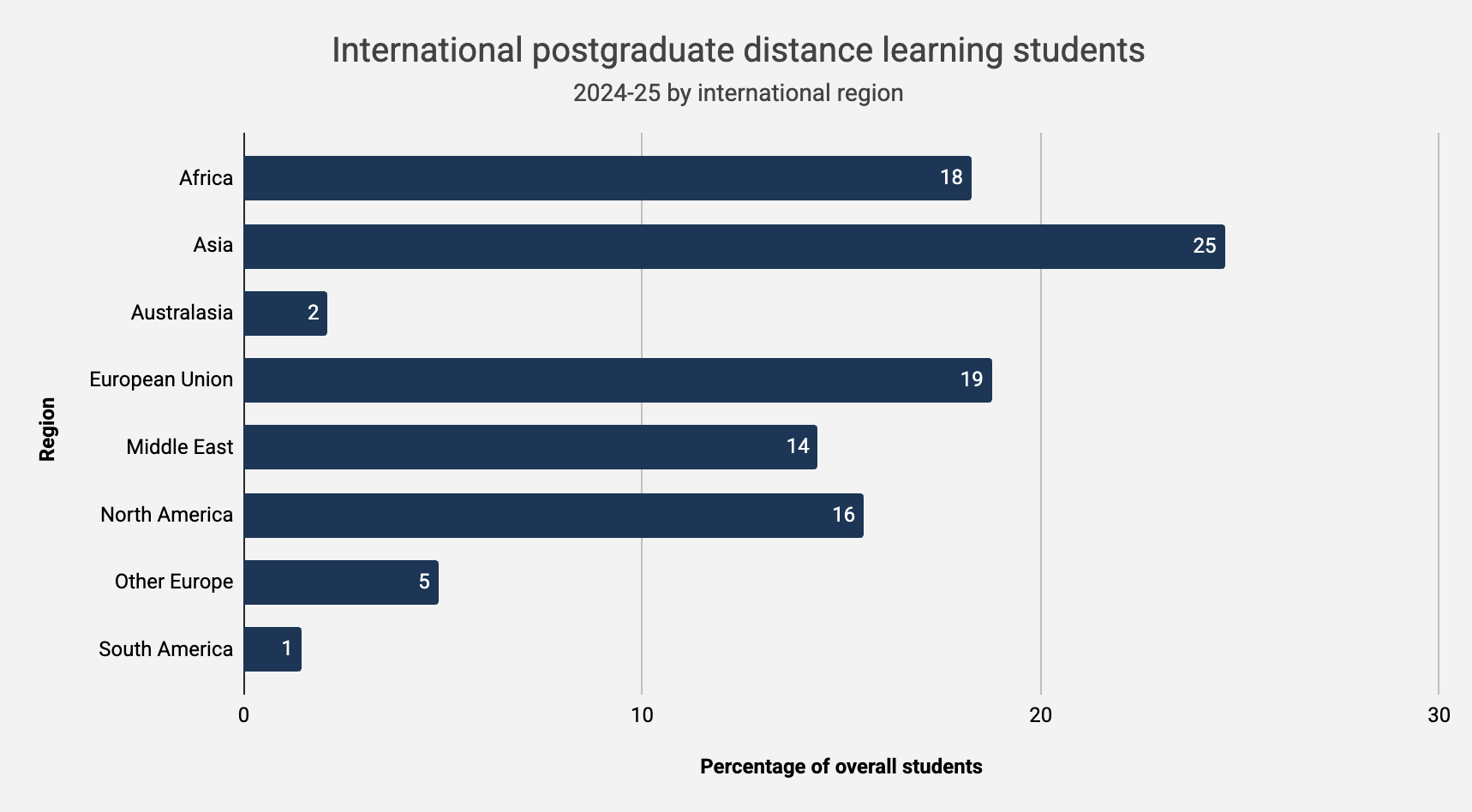

The online international postgraduate degree landscape differs in some respects from the undergraduate market. It is less concentrated by international region and, although Asia has the largest number of students, this accounts for just under 25%, compared with over 50% of online undergraduate degree students. Similarly, there is less concentration among a small number of universities, with the 2024–25 data showing 26 institutions enrolling over 900 online TNE postgraduate degree students.

The regions that have shown the most significant growth in student numbers are again Asia and the Middle East, but the more striking story in terms of student numbers by region is the substantial decline in the number of EU students. Since 2020–21, the number of online postgraduate students based in the EU has fallen by nearly 7,000.

Now, at this stage, I can guess what you're thinking, and the exact B word that is on your lips. However, this is one of those rare instances where the decline is largely attributable to a single factor. Specifically, it reflects a reduction of nearly 7,000 students at the University of South Wales since 2020–21. This is largely due to the cessation of a partnership, and without going into detail, and although this might sound odd, it is highly likely that the majority of these students were not actually EU students but were simply registered there. In reality, the number of online TNE postgraduate students in the EU has remained fairly stable over this period. This underlines the risks of interpreting data without triangulating it with deeper research and contextual knowledge.

International online postgraduate students by provider

There is a much broader spread of UK universities with significant student numbers, with 26 institutions recording over 900 students in 2024–25 and no single dominant provider. Overall, there have been mixed fortunes among those institutions with the largest numbers of online TNE PGT students, with some experiencing significant increases or decreases and others seeing minimal change.

Those universities recording the most significant increases, defined as over 250 students, include the University of Buckingham, the University of Liverpool, the University of Sussex, Arden University and the University of Essex Online. For some of these institutions, this represents a continuation of growth over several years.

Several institutions reported significant declines in student numbers, and a number appear to be on a multi-year downward trend. These include the University of Salford, the University of Manchester, the University of Sunderland, the University of South Wales, SOAS, University of London, and Queen Mary, University of London. The largest decreases in student numbers were at the University of Sunderland, Edinburgh Napier University and Northumbria University.

In terms of overall student numbers, the following were the top ten UK universities in 2024–25.

Top UK universities by number of international online postgraduate students

University of London - 6,870

King's College London - 4,510

University of Salford - 4,250

University of Edinburgh - 2,995

University of Manchester - 2,730

Heriot-Watt University - 2,465

University of Essex Online - 2,300

University of Sunderland - 2,030

University of Reading - 2,025

University of Liverpool - 2,010

The only change from last year is the University of Liverpool, which has a long history of enrolling large numbers of international online PGT students, rejoining this group after substantial declines in numbers during the 2010s.

Overall reflections on TNE online student enrolments

When considering online TNE student numbers and the trends this data presents, both at a macro and individual provider level, it is important to recognise that there is a great deal of nuance that numbers alone cannot convey. Trends and fluctuations across providers represent different realities. For some, increases are driven by prioritisation, investment, performance and partnerships, while for others, declines are the consequence of factors such as international online partnerships coming to an end.

In general terms, I would strongly caution against thinking of the TNE online student landscape as a kind of homogeneous global B2C market. The student numbers presented here are not solely indicative of universities acting independently to attract international students to their existing online programmes. In several cases, the numbers reflect an almost B2B approach, arising from relationships with overseas providers, or are largely dependent on regional affiliates or internationally focused online education companies.

Overall, similar patterns prevail in the international online student landscape as in the UK market. There are relatively few providers genuinely invested in online undergraduate provision, but those that are, and have been over the longer term, are either growing enrolments or sustaining them at reasonable levels. Although the University of London has a very large number of online undergraduates, several other universities have grown their cohorts into the thousands and have been increasing student numbers at a faster rate.

The international online postgraduate student landscape is perhaps the most interesting. Over the last ten years, it is clearly evident that a number of UK universities have expanded their international online student numbers. This has been achieved through a combination of broader online market entry, enrolling both international and UK students, and more targeted international initiatives such as partnerships.

Given the growing competitiveness amongst UK HE providers offering online degrees, international student markets present an obvious route when seeking to achieve and sustain sufficient numbers of online students. There has definitely been more effort and emphasis on recruiting international students to online programmes by a range of institutions and also online programme management (OPM) companies in recent years.

This aligns with the wider trend of increased investment in TNE among UK HE providers. Alongside this, there have been developments such as the QAA receiving government funding to secure recognition of transnational distance learning provision in certain countries, the British Council developing strategies to support further TNE growth, and Jisc beginning to report on the digital experiences of TNE students. It is not just HE providers but other organisations in the wider ecosystem that are seeking to get a piece of the growing focus on TNE.

While none of these developments are negative, it strikes me that there is little out there to really support institutions in seeking to grow and develop financially viable and sustainable cohorts of online TNE students either directly or indirectly. This concern is reinforced by the limited discussion among TNE stakeholders of a significant commercial challenge to online TNE growth, and potentially to the ambitions set out in the UK’s most recent international education strategy, which is the impact of countries’ Goods and Services Tax. These vary by country, but in some cases exceed 20%.

Universities are taking different approaches on this at the moment with some applying the tax to student fees at the relevant rate for their home country, while others are absorbing the cost themselves. Either way, this adds to fees in what is already a highly price-sensitive market, or places pressure on institutional financial sustainability.

While it is great that the Department for Business and Trade is funding organisations such as the QAA to secure recognition of distance learning in other countries, the department should also consider what action might be taken in relation to the Goods and Services Tax on distance learning exports. However, the absence of attention in this area speaks to the broader sense that there is greater emphasis and knowledge centred in other forms of TNE than on online provision.

In summary, the latest data supports the wider trend of increasing focus on TNE, with some institutions clearly expanding international online student recruitment. However, growth is far from uniform, and this continues to be an area where it’s easy to hype up potential and much harder to deliver long-term sustainable success.